SNR – GST UPDATE

Recently Karnataka AAR has given a ruling in the matter of “Mr. Anil Kumar Agrawal” holding that salary paid to executive director is not liable to GST as it is covered under schedule III of CGST Act, 2017, thus not to be considered for computing aggregate turnover for registration. This ruling has effectively put aside the confusion of applicability of GST under RCM on director’s remuneration ruled in Rajasthan AAR in the matter of “Clay Craft India Private Limited”. Brief facts and findings of the present ruling are analysed in this update.

FACTS & QUESTION BEFORE THE AAR

- The applicant is an unregistered person and was earning income from various sources such as salary from partnership firm, Salary as director from Private Limited Company, Rental income, interest & Income from different

- The applicant wants to know which all revenue/income shall be considered for Aggregate Turnover for registration & does exempt income shall also be reckoned for the

AAR DISCUSSION & FINDINGS

In this regard AAR referred the definition of “aggregate turnover”, in terms of section 2(6) of

the CGST Act,2017, which means:

Aggregate value of all

- taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis)

- exempt supplies

- exports of goods or services or both

- inter-State supplies of persons having the same Permanent Account Number

to be computed on all India basis but excludes central tax, State tax, Union territory tax, integrated tax, and cess.

Based on the above definition, AAR findings on the various types of income to be included in aggregate turnover or not are as follows:

| S.NO. | TYPE OF INCOME | AAR REMARKS |

| 1. | Interest income received from different sources | Interest income arising out of the deposits/loans extended are exempted under entry no 27(a) of the notification No.12/2017-Central Tax (Rate). To be

included in aggregate turnover. |

| 2. | Partner’s salary received as partner, from applicant’s partnership firm | In case applicant is a working partner and is getting salary, then the said salary is neither supply of goods nor services in terms schedule III of CGST Act, 2017.

Thus not to be included in aggregate turnover. |

| 3. | Rental income on commercial property | The transaction amounts to supply in terms of section 7(1)(a) of CGST Act,2017. Thus, to be

included in aggregate turnover. |

| 4. | Rental income on residential property | The transaction amounts to supply but the same is exempted in terms of entry no 12 of Notification No

12/2017. Thus, to be included in aggregate turnover. |

| 5. | Life Insurance Policy Maturity receipts | After completion of the insurance contract, no service is involved between policy holder and insurance company and hence not to be included in

aggregate turnover. |

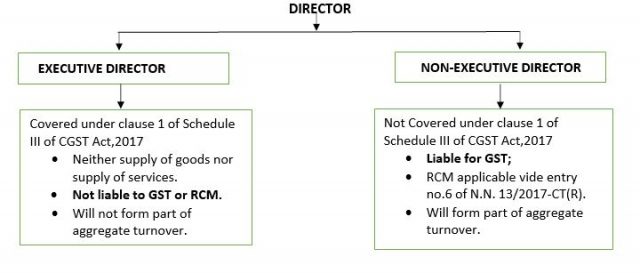

- Salary paid to Director

In the aforesaid ruling, AAR has squarely dealt with the taxability of remuneration paid to directors. It has gone on record to differentiate the GST treatment of remuneration paid to non-executive directors and executive directors. The present ruling has confirmed the tax position been taken/ suggested by GST experts even after the contrary ruling by Rajasthan AAR in the matter of Clay craft India Private Limited. The ruling of AAR has also explained the inclusions and exclusions in aggregate turnover of various heads of income which would help businesses (specially Individuals) to decide their GST registration & thereon compliance requirements.