What is Corporate Guarantees?

If we understand in simple terms, it is a guarantee given by a firm/corporate/body corporate (known as Guarantor) on behalf of another person or entity for a loan obtained by such person. In case of default by the borrower, the guarantor undertakes to repay the loan. This arrangement provides assurance to the lender and mitigates credit risk. Such guarantees are commonly observed in group structures, particularly between holding and subsidiary companies.

Can a guarantee given without any consideration still attract GST?

Actually Yes. Where a guarantee is provided for a consideration, it clearly qualifies as a supply of service under the GST law. However, even in cases where no consideration is charged, the transaction may still be liable to GST if it is between related persons.

In terms of Schedule I of the CGST Act, 2017, supply of goods or services between related persons, even without consideration, is deemed to be a supply. Accordingly, corporate guarantees extended within group entities fall within the ambit of GST, notwithstanding the absence of consideration.

However, as clarified in circular 204/16/2023-GST, if guarantee is provided by Director to a company then value of supply will be considered as Nil although they are related party under GST Act. This is due to the restriction by RBI, RBI’s Circular No. RBI/2021-22/121 dated 9th November, 2021, no consideration by way of commission, brokerage fees or any other form, can be paid to the director by the company, directly or indirectly, in lieu of providing personal guarantee to the bank for borrowing credit limits. As such, when no consideration can be paid for the said transaction by the company to the director in any form, directly or indirectly, as per RBI mandate, there is no question of such supply/ transaction having any open market value. Accordingly, the open market value of the said transaction/ supply may be treated as zero and therefore, taxable value of such supply may be treated as zero. In such a scenario, no tax is payable on such supply of service by the director to the company.

What shall be the value of guarantee provided?

In the absence of consideration, reference is required to be made to Section 15 of the CGST Act read with Rule 28 to Rule 32 of the CGST Rules, which provides that the value shall be determined based on the open market value or value of like kind and quality.

Given the practical challenges and ambiguity in valuation, the Government has issued specific clarifications by Notification No. 52/2023 –Central Tax dated the 26thOctober, 2023 prescribing a deemed valuation mechanism for corporate guarantees provided between related parties.

Notification states that ‘Notwithstanding anything contained in sub-rule (1) of rule 28, the value of supply of services by a supplier to a recipient who is a related person, by way of providing corporate guarantee to any banking company or financial institution on behalf of the said recipient, shall be deemed to be one per cent of the amount of such guarantee offered, or the actual consideration, whichever is higher.’

To better understand the implication of the above provision, consider the following illustration:

Illustration:

A holding company provides a corporate guarantee of ₹100 crore to a bank on behalf of its subsidiary without charging any consideration.

In such a case, the value of supply shall be deemed to be 1% of ₹100 crore, i.e., Rs.1 crore. Accordingly, GST would be payable on ₹1 crore, despite no actual consideration being charged.

And if Consideration charged by holding company is say Rs. 2 crores then , the value of supply shall be deemed to be higher of

- 1% of ₹100 crore, i.e., ₹1 crore, or

- Consideration chaged i.e. Rs. 2 crores.

This deemed supply significantly alters the tax position, as tax liability arises even in the absence of any real income.

On 10 July 2024, CBIC issued a notification amending Rule 28(2) of the CGST Rules by inserting the words ‘per annum’ after ‘amount of such guarantee offered’, with retrospective effect from 26 October 2023. Accordingly, the taxable value of a corporate guarantee shall be computed at 1% per annum of the guaranteed amount for the duration of the guarantee.

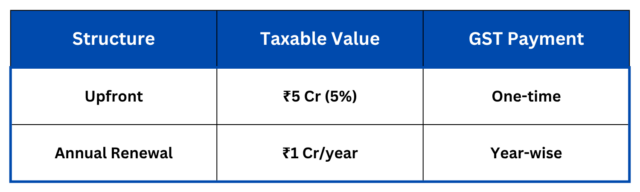

As clarified in Circular No. 225/19/2024-GST, the timing and valuation of GST on corporate guarantees depend on the structure of the guarantee. Where a guarantee is issued for the entire tenure upfront, GST is payable upfront for the full period.

For instance, for a guarantee of ₹100 crore with a tenure of 5 years and no consideration, the taxable value would be ₹5 crore (5%) if issued upfront, with GST payable in one instance, whereas in case of annual renewal, the taxable value would be ₹1 crore per year, with GST payable annually. For guarantees covering a partial period, valuation is to be computed proportionately (e.g., 0.5% for six months)

Illustration

- Guarantee Amount: ₹100 Cr

- Tenure: 5 years

- Consideration: Nil

Through their Circular No 225/19/2024-GST, GST department also clarified that recipient of the service of providing corporate guarantee shall be eligible to avail the ITC, subject to other conditions specified in the Act and the Rules made thereunder, irrespective of when the loan is actually disbursed to the recipient, and irrespective of the amount of loan actually disbursed.

The introduction of a deemed valuation mechanism has impacted the business in following manners:

- Taxability without income: GST liability arises even where no consideration is charged, leading to a disconnect between tax and actual revenue.

- Increased compliance burden: Companies are now required to identify and report such guarantees and discharge GST accordingly.

- Working capital impact: Tax needs to be paid on notional value, resulting in cash flow strain, especially in large-value guarantees.

Impact on group structures: Common treasury functions and intra-group financial support arrangements may need re-evaluation.

Lets address some common issues or questions related to corporate guarantee: