SNR – GST Update

Central Board of Indirect Taxes & Customs (CBIC) has issued two circulars on 10th June 2020 to issue clarifications regarding refund of accumulated ITC relating to imports, ISD invoices & inward supplies liable to RCM and GST applicability on Director’s remuneration. These circulars have provided much needed clarity on both the issues to the trade as well as GST department. We have discussed the clarifications issued in this update.

1. Circular No. 139/09/2020-GST dated 10 June 2020

Circular No 135/05/2020- GST dated 31st March 2020 was issued which inter alia denies the refund of ITC on inward invoices which are not reflecting in Form GSTR-2A. Due to this, department officers were not allowing even the refund of ITC availed on Imports, ISD invoices and RCM supplies due to non-reflection in GSTR-2A. Now, CBIC has clarified that the restriction imposed by Circular dated 31st March 2020 shall not apply on refund of ITC availed on invoices relating to imports, ISD invoices and RCM supplies even if they are reflected in GSTR-2A.

2. Circular No. 140/09/2020-GST dated 10 June,2020

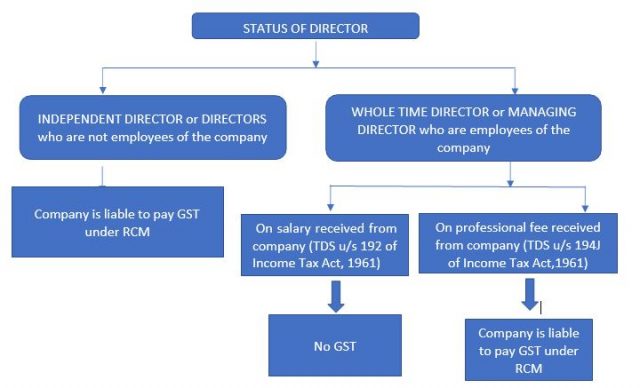

Through this circular, taxability of remuneration paid to Directors which has created a lot of hue and cry among the trade and industry due to the Rajasthan AAR ruling in the matter of “Clay Craft India” in which it was held that remuneration paid to director (whether whole time or independent) shall be taxable under GST on RCM basis. Tax position emerging after circular is represented in the below chart:

SNR COMMENTS

Both the circulars would be very helpful in removing various confusions prevailing in industry about GST refunds and taxability of remuneration paid to directors. The refund circular is important as the GST officials are strictly adhering the previous circular no. 135 which talks about ITC reflected in GSTR- 2A without considering the admissibility of credits on account of imports, ISD, RCM supplies.

In case a company enters into an employment service agreement with a Director and he works as Managing Director or Whole Time Director, then the remuneration paid to him shall not be a supply and would not be covered under reverse charge mechanism due to existence of employer-employee relationship. Further, remuneration paid to independent directors, who are not employees of the company is taxable in the hands of the company under reverse charge (RCM) basis.